The $3,250 gym membership

A new status symbol?

I’m an avid gym-goer. I pay €100/month for what’s considered a “premium” gym here in Munich — and let’s be honest, the only premium feature is the towel. (Okay, and the central location.)

Meanwhile, in cities like New York and Los Angeles, a new kind of “wellness club” charges $3,250+ per month — that’s $39,000 a year. The trend has already hit London, and it’s probably fair to assume it will spill across the English Channel into continental Europe next.

So, I wanted to understand what’s really happening. Is this a bold new business model—or a market overheated by hype?

The rise of the social wellness club

New concepts like Barry’s bootcamp, and boutique studios like cycling and Reformer pilates with average €30 per class have been challenging the traditional gyms in the recent years. But we’re now in a new tier entirely: hyper-luxury social wellness clubsthat blend biohacking, spa, and community.

Some standout examples that I found when doing my research (and more examples in the table below):

Remedy Place (New York, Boston, LA): Membership starts at $550/month ($3,250/month for full access), with services like IV drips, lymphatic drainage, and “social ice baths.”

The Well (New York & Miami): Up to $4,500/year for all-access memberships that include Ayurvedic doctors, meditation domes, and infrared saunas.

Surrenne (London): Housed under the new Emory Hotel in Knightsbridge, memberships start at £10,000 per year, with a £5,000 joining fee.

Why now?

Luxury wellness clubs didn’t appear out of nowhere — they’re riding the wave of deeper shifts in status, identity, and spending behavior. A few core drivers:

Health is the new wealth: 82% of Americans now say wellness is a top or important priority in their daily lives.

Exclusivity sells. In an era where luxury logos are everywhere and social media can fake almost anything, real status comes from what’s not accessible. Many of these clubs require referrals or rigorous vetting. Surrenne caps its membership at 100 people. Continuum in New York reportedly limits theirs to just 250.

The billionaires are doing it. Bryan Johnson spends $2M/year reverse-aging himself. Jeff Bezos backed a longevity startup—Altos Labs—which has raised $3B in funding. If the world’s richest men are biohacking, who’s going to shame you for a €400 vitamin drip?

In a post-pandemic world, self-care got rebranded as optimization. Self-care used to mean a face mask. Post-pandemic, spending on physical and mental wellness is no longer a guilty pleasure — it’s a signal of productivity, discipline, and ambition. Taking care of your nervous system is framed not as self-care, but as performance optimization.

Tailwinds behind the boom

These consumer behaviours are translating into tangible trends that fuel the growth of social wellness clubs. The social wellness club business model sits at the intersection of three distinct—and rapidly expanding—markets:

Experiential > product luxury: Spending on experiences grew by 5%, while luxury goods saw a 2% decline.

Wellness mega-trend: The global wellness economy reached $6.3 trillion in 2023 and is expected to hit $9 trillion by 2028.

Members' club come-back: The private members’ club market is expected to grow at an 11% CAGR, reaching $26 billion by 2027.

Business model: still in beta

No one’s cracked the blueprint yet.

Is it a spa with a social calendar? A café with an IV drip menu? A tech-powered retreat with concierge breathing?

Some clubs lean hospitality. Others go full diagnostics. A few are still figuring out if they’re running a schedule—or letting members freestyle with cryo and sound baths.

What’s clear: This isn’t your old-school gym model—sell a ton of subscriptions and pray no one shows up. Social wellness clubs are built on presence, not absence.

You come often. You stay longer. You bring friends and you make friends. The margins are made in the community.

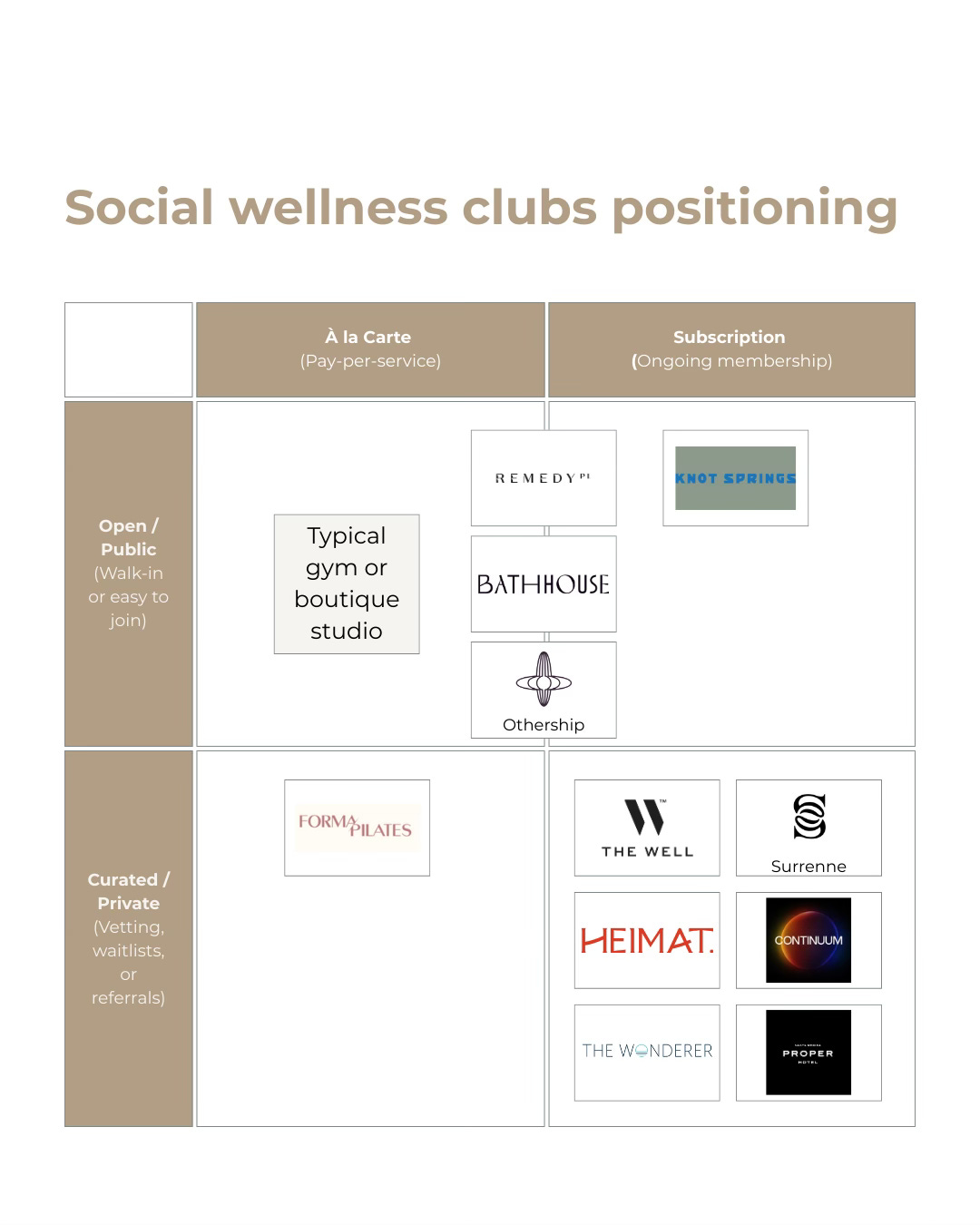

Here’s one way to frame how these clubs are diverging (on a 2×2, of course :)):

Business model challenges

I think it’s a complex business model—with clear appeal, but also real constraints. Like most location-bound concepts, scalability is limited. Still, the category is gaining traction, and I expect we’ll see more of these clubs backed by serious capital as investors test the waters.

Here’s why it’s challenging:

CapEx & operating costs: From interiors to equipment to staffing, the expectation for a premium experience drives both upfront investment and ongoing operational complexity.

Scaling: What makes these clubs desirable—their intimacy, curation, and in some cases founder-led feel—is also what makes them hard to replicate. You can’t franchise cool or clone social cachet across cities.

Operational complexity: These aren’t just gyms. They’re part spa, part hospitality venue, part diagnostic clinic. Running one well requires a rare mix of wellness expertise, service design, medical compliance, hospitality, etc.

How the model could scale

Despite its challenges, there are clear paths to making the social wellness club model more scalable—and, in turn, more investable. Here are a few ideas worth watching:

Data loops: Membership-based businesses already benefit from recurring revenue. But in wellness, retention can go beyond habit or inertia. Integrating health tracking (via wearables, blood panels, etc.) allows for personalized services, measurable outcomes, and a stronger case for long-term renewals.

Hospitality partnerships: Some brands are embedding within five-star hotels, reducing real estate exposure while tapping into built-in foot traffic and luxury clientele.

Signature programs or products: A few clubs are beginning to launch their own supplements, branded content, or virtual wellness programs—extending the brand beyond the physical space and adding new revenue streams that are easier to scale.

So: Would you spend $3,250/month for a gym?

Will your answer change if it included a hand-picked community, IV therapy, and member-exclusive dinner?